Aave v4 的一些思考:是否每个大协议都应该发条链?

X,@cmdefi报道

针对Aave v4的一些重要变化和规划,BV DAO创始人陈默进行了总结。其中一些问题早已被改进,但也有一些看似坚持DeFi老路线的规划。在这其中,我们不禁要问,每个大型协议是否都应该有自己的链?

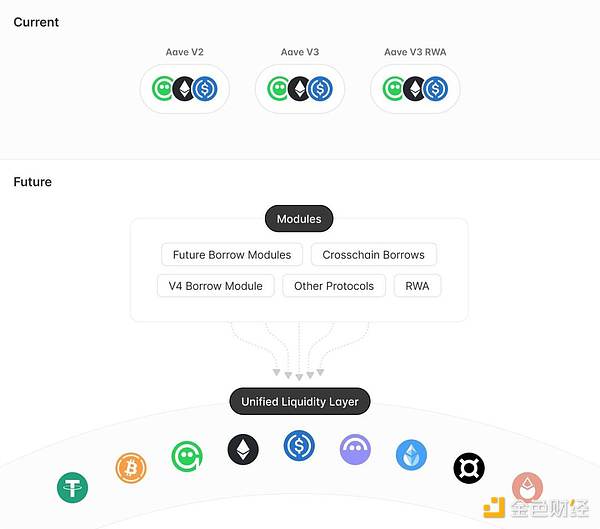

1. 统一流动性管理

将所有资金供给和借出集中管理,以确保流动性不会分散在不同模块中。

允许协议在未来方便地添加或移除功能模块,而不需要迁移流动性,为长期扩展提供了便利。

最大的好处在于不再需要在Aave V2/V3/V4之间来回切换选项卡,也不需要像V3升级时手动将资金从V2迁移到V3。

2. 模糊控制利率功能

Aave V4提议采用全自动利率,能够调整利率曲线的斜率。目前的设定由治理机制控制,增加了治理负担,同时也降低了资本效率。模糊利率设计旨在主动控制利率曲线的转折点,使其根据市场状态动态调整。基本利率将根据市场需求上升或下降,以此优化供应者与借款人的利率。

这一点是早就应该优化的,笨重的利率模型和冗长的治理流程已经让Aave备受煎熬。在之前$CRV被恶意做空事件中,Fraxlend就已经以算法控制利率遥遥领先,高风险时优先偿还利率模型更健康的Fraxlend借款。

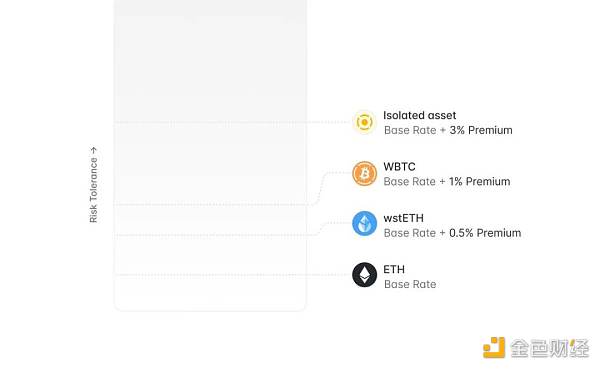

3. 流动性溢价机制

V4引入了“流动性溢价”概念,根据抵押资产的风险状况(如中心化程度、市场风险等)动态调整借款利率。面对较高风险的抵押品,借款成本相对提高;反之,风险较低则有助于降低借款成本。

这是一个相当不错的风险管理功能,许多山寨币仍然在链上需要借贷,风险分级是一种合理策略。

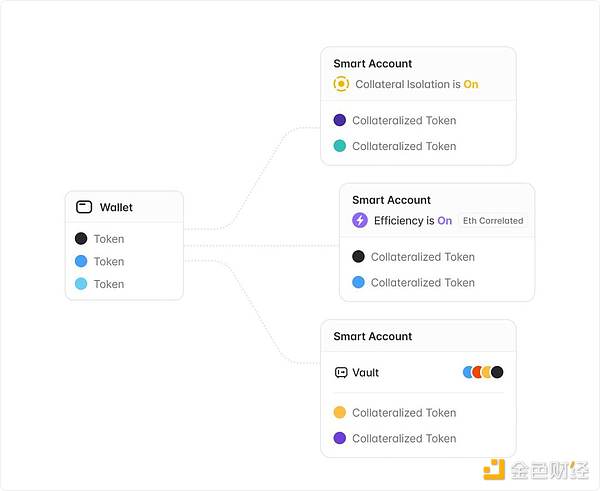

4. 推出智能账户(Smart Account)和金库(Vault)

此举大幅改善了用户体验,允许用户通过单一钱包管理多个头寸。智能账户解决了V3的一个主要用户体验问题:使用e-mode或隔离资产借款时,需要使用多个钱包管理头寸的烦恼。

引入智能账户后,用户可以在一个钱包中创建多个子账户,大大简化了与协议的交互。智能账户还满足了用户对“金库”功能的高需求。用户可以在智能账户中抵押资产借款,抵押品被锁定但不会进入流动性池,从而降低了风险。

这也是一个非常好的体验升级,早该出现。

5. (未完,待续)

动态风险参数配置

Chen Mo, the founder of the report, summarized some important changes and plans, some of which have already been improved, but there are also some plans that seem to adhere to the old route. Among them, we can't help but ask whether each large-scale agreement should have its own chain, unified liquidity management, and centralized management of all funds supply and lending to ensure that liquidity will not be dispersed in different modules, allowing agreements to easily add or remove functional modules in the future without moving liquidity, which has facilitated long-term expansion. The biggest advantage is that there is no need to switch tabs back and forth between them, and there is no need to manually transfer funds from to fuzzy control interest rate function when upgrading. It is proposed to adopt automatic interest rate to adjust the slope of interest rate curve. The current setting is controlled by governance mechanism, which increases the governance burden and reduces the capital efficiency. The fuzzy interest rate design aims to actively control the turning point of interest rate curve so that it can dynamically adjust the basic interest rate according to market conditions, so as to optimize suppliers and suppliers. The borrower's interest rate, which should have been optimized a long time ago, is a cumbersome interest rate model and a lengthy governance process, which has made it hard to control the interest rate by algorithm in the event of malicious short selling before. The healthier loan liquidity premium mechanism introduces the concept of liquidity premium, and dynamically adjusts the loan interest rate according to the risk status of mortgaged assets, such as centralization, market risk, etc. In the face of higher-risk collateral, the cost of borrowing is relatively higher, and vice versa. Lower borrowing cost is helpful to reduce borrowing cost, which is a pretty good risk management function. Many shanzhai coins still need to borrow in the chain. Risk classification is a reasonable strategy. Introducing smart accounts and vaults has greatly improved the user experience, allowing users to manage multiple positions through a single wallet. Smart accounts have solved a major user experience problem. When using or isolating assets, they need to use multiple wallets to manage positions. After introducing smart accounts, users can create more than one wallet. The sub-account greatly simplifies the interaction with the agreement, and the smart account also meets the high demand of users for the vault function. Users can mortgage assets, loans and collateral in the smart account, but they will not enter the liquidity pool, thus reducing the risk. This is also a very good experience upgrade. It is long overdue for dynamic risk parameter configuration. 比特币今日价格行情网_okx交易所app_永续合约_比特币怎么买卖交易_虚拟币交易所平台

支持为单个资产创建独立的风险配置,降低清算风险。引入自动化资产下架机制,简化治理流程。

- V3 的风险参数调整 ( 尤其是清算阈值 ) 影响所有用户,降低阈值可能引发不必要的清算,治理成本高。

- V4 引入动态配置功能,新的借款使用新配置,已有用户仍使用原有配置。

- 配套推出自动化资产下架机制,治理层触发后,系统逐步调低资产的清算阈值直至归零,效果相当于该资产无法再完成借贷业务,等同于人工下架但简化了治理流程。

引入超额债务保护机制,防止不良债务扩散

共享流动性模型的一个弊端是资产积累超额债务会传染,V4 引入新机制追踪资不抵债头寸,自动核算累积的超额债务,当超额债务超过既定阈值,相关资产自动失去借款能力,防止坏账扩散。

提供与 GHO 稳定币的原生集成

- 支持在流动性层原生铸造 GHO。

- 引入 GHO「软清算」AMM,仿照 crvUSD。

- 引入 GHO 紧急赎回机制,应对极端脱锚情况。

- 允许存款人选择以 GHO 形式获取利息,协议将利息转换为 GHO 的抵押品,增强 GHO 稳定性。

Aave Network

Aave宣布计划推出全新的网络层,将作为GHO稳定币和Aave借贷协议的核心枢纽。

将采用GHO支付费用。

以Aave V4为核心。

$AAVE将作为去中心化验证者/排序器的主要质押资产。

通过Aave Governance V3由社区控制该网络与以太坊的接口和交互。

广泛使用账户抽象。

继承自以太坊的网络安全性。

Aave Labs表示将持续关注一层和二层网络的发展,并为Aave社区选择最适合的技术方案。

关于Aave Network,有一种目前DeFi行业的倔强气息。从目前公布的信息和状态来看,似乎这是一个连团队自己都尚未明确的决定:是选择一层(Layer 1)还是二层(Layer 2)?如何选择?是否真的有必要?对于这些问题,仍存疑。

但唯一较为明确的是,Aave未来将继续致力于稳定币市场,所有规划都将围绕着GHO场景展开。

由于当前应用层创新的匮乏,似乎正处于基础设施牛市之中。每个项目都不好意思去融资,若没有一层(Layer)存在。而DeFi协议一旦扩大,是否真的有必要去开发一条新的区块链,目前看来仍然不确定。从我的观点来看,以太坊似乎是金融活动的核心所在。对于一些并不过分依赖性能的项目而言,离开以太坊自建区块链可能并不能为用户带来更多的好处,反而可能降低初始阶段的安全性。

注册有任何问题请添加 微信:MVIP619 拉你进入群

打开微信扫一扫

添加客服

进入交流群

1.本站遵循行业规范,任何转载的稿件都会明确标注作者和来源;2.本站的原创文章,请转载时务必注明文章作者和来源,不尊重原创的行为我们将追究责任;3.作者投稿可能会经我们编辑修改或补充。