比特币生态崛起会削弱以太坊吗?它的价值又将如何体现?

近期比特币生态崛起迅速,由于部分路线可能会和以太坊生态重合引发部分加密社区的担忧,那么比特币生态崛起真的会削弱以太坊吗?其实未必,以太坊也有自己独特的价值体现…..

不可否认,当前互联网的发展给我们带来了无尽的丰富。但它缺少两个关键要素:

互联网用户没有数字产权。

互联网没有一个可信的中立、共享、安全、无需许可的全球会计系统——来记录用户的状态并在一个共享账本上实现全球贸易。

而这两点恰好是是区块链的核心价值主张,互联网的革命在到来的路上。

以太坊的构建反映了互联网的构建

比特币是第一个公共区块链。在早期,如果您想利用这一新的技术突破创建一个新的应用程序,您必须启动自己的区块链。例如一开始Namecoin(点对点命名系统)是比特币网络的一个分支。这个公共区块链时代类似于互联网早期,你必须托管自己的服务器来构建网站。

以太坊于 2015 年创立,它被创建为“公共区块链的地理城市”,以太坊能让开发人员利用共享基础设施来构建基于区块链的应用程序,而且更便宜、更高效。

然而,为特殊用例构建应用程序需要很大的灵活性。进入 L2 和特定应用程序区块链使得大家开始在以太坊“之上”构建执行服务,而以太坊作为基础层结算基础设施。

于是以太坊正在成为一个“网络的网络”。就像互联网一样。L2 看起来与淘宝服务非常相似——在维护共享基础设施的同时实现灵活性和可扩展性。

此外,L2 的增强可扩展性正在与零知识证明一起开发,这为公共区块链带来了隐私——就像 HTTPS 为互联网带来加密,从而实现电子商务一样。

以太坊的商业模式

投资者应该将以太坊网络视为两个不同的事物:

ETH – 为网络提供运行动力并为其以去中心化方式运行创造经济激励的原生Token。

以太坊——计算网络和会计系统,作为其他企业在“之上”构建应用程序的基础层基础设施。

1)数据概况

非零地址:过去8年来,累计总数呈指数级增长。截至2023年9月30日,增长超过1.07亿个,较一年前增长了26%,与上季度比增长了4.9%。

活跃地址:在第三季度,以太坊的平均每日活跃地址约为40万,较上季度下降4%,类似的下降现象在去年的加密货币低谷期也出现过,但随着市场情况改善,新用户开始涌入。

平均日交易量:第三季度,以太坊日均交易量略有增长,网络需求持续超过供应,而随着网络规模扩大,L2网络(如Optimism、Arbitrum和Base)正在处理更大比例的交易,L2上的交易量在过去几年增长超过3438%,突显了以太坊网络中摩尔定律的作用。

平均开发人员数量:在以太坊上工作的平均核心开发人员数量在第三季度趋于平稳。根据 Electric Capital 的开发者报告,以太坊生态系统拥有超过 5946 名活跃开发者,在过去两年中增长了 51%,是其最接近竞争对手的 3 倍多。请注意,这些数字可能被低估,因为它们没有反映对以太坊上构建的专有加密业务的任何贡献。

每日平均 Gas 使用量:平均 Gas 使用量作为以太坊 L1 上的区块空间需求指标,与每日交易量类似,近期略有增加;自网络成立以来,Gas 限制已增加了5倍,每次增加都是为了满足块空间需求,预计这种关系将持续,进一步发展L2解决方案,扩展以太坊的计算资源。

平均交易费用:以太坊第三季度平均交易费用为4.85美元,较上季度下降46%,表明在高需求时区块空间供应不足导致费用激增,而网络通过L2解决方案和侧链(如Arbitrum、Optimism、Base和Polygon)进行扩展,利用L2的应用程序的交易成本低至1美分至13美分不等;预计EIP4844的实施将进一步降低第四季度的费用。

ETH质押:ETH质押率的增长对以太坊网络健康发展至关重要,该指标追踪着网络中被质押的流通ETH百分比,随着质押参与度的急剧上升,ETH持有者逐渐展现了长期前景,ETH目前是唯一实现正实际权益率(3.6%)的公共区块链网络。

ETH 价格:加密市场呈现极强的反射性,ETH价格与链上指标密切相关,展示了自2015年以来每年剧烈波动,例如2018年的价格底部83.79美元和2021年的57倍增长峰值,后文将提供更深入的估值分析。

日交易量:第三季度交易量持续下滑,与去年同期相比下降了56%,而与监管不确定性有关的Jane Street和Jump Trading在美国市场的做市业务缩减,同时随着加密货币寒冬持续,散户投资者对该领域失去了兴趣。

TVL(美元):以太坊DeFi应用中 TVL 为39亿美元,较上季度下降12%,但依然比最接近的竞争对手高出5.8倍;TVL另一视角是“管理下的资产”,目前智能合约中持有的ETH比例达32%,创历史新高,显示管理资产的健康状况。

单位经济效益:每个活跃地址的每日收入在第二季度较上季度增长87%,但较22年同期下降24.9%,显示活跃用户每日费用增长与交易费用增长一致,表明网络拥堵时用户愿意支付更高费用,因为链上交易的时间价值和敏感性。

通过L2解决方案,我们看到用户费用大幅下降。当这种情况发生时,交易量预计将呈指数级增长。

2)商业模式

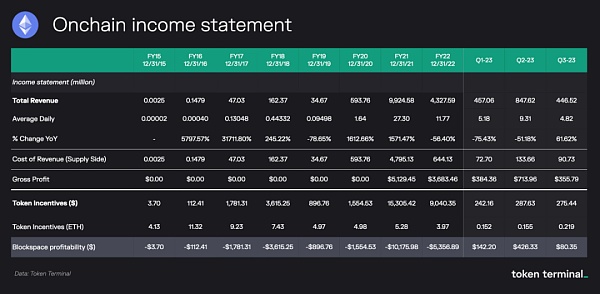

尽管以太坊的经济和市场结构去中心化,但其商业模式简单,收取少量计算/结算费,随着应用扩大,网络变得越来越有利可图,接下来详细分析了以太坊的财务状况。

总收入:以太坊的交易费用指用户在网络上支付的总费用,预计未来应用程序将代表用户支付费用,涵盖点对点支付、DeFi贷款、交易平台交易、游戏体验、NFT铸币等任何利用以太坊区块链的操作,而使用2解决方案的应用程序最终将结算数据为以太坊基础层的交易,尽管第三季度收入较第二季度下降47%,但网络仍然实现盈利。

收入成本:此行项目代表支付给供应方(验证者)的金额,验证者通过批准交易和确保网络安全为网络提供服务,其中80%的用户费用在本季度被烧毁,剩下的20%代表优先费和MEV成本。

Token激励:Token激励代表网络支付给验证者的区块补贴,在2022年的“合并”后,以太坊的安全费用大幅降低了87%,使网络进入盈利状态,为验证者和被动持有者提供了用户费用的补偿。

对于Token激励存在不同观点,普遍看法认为它是网络支付给验证者的一种“费用”,但其实质不同于传统意义上的费用,因为验证者并非直接支付这笔奖励,这一概念在当前情况下可能难以精确量化。

区块空间盈利能力:从链上角度看,本季度以太坊的净收入为7870万美元,较第二季度下降81%,尽管减少,但以太坊仍是唯一盈利的公共区块链,因为用户费用超过了网络Token激励的费用。

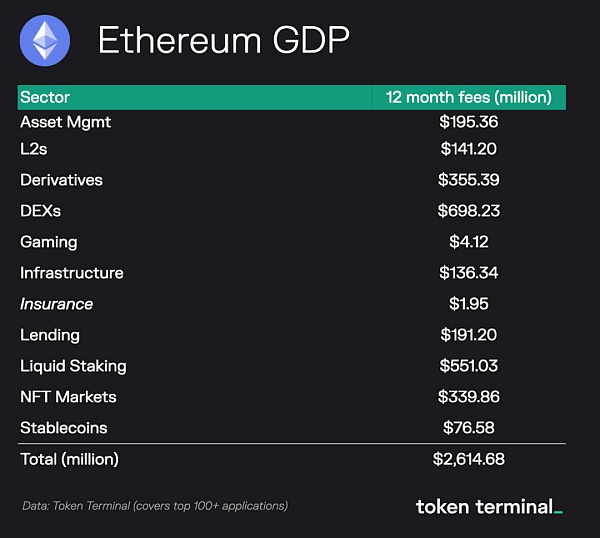

相对估值:“GDP”分析

比较以太坊相和其他L1网络估值的一种方法是使用“GDP”分析。在这种情况下,我们将量化和预测网络的经济机会或 GDP。区块链网络的 GDP 是构建在 L1 之上的应用程序产生的所有收入的总和。

从这个角度来看,我们将L1区块链视为“国家”,而不是网络或公司。一个国家的货币的强弱取决于其经济/GDP、产权和法律体系(国家的基础设施)以及对货币的需求(纳税、购买商品、消费服务、储值等)。)

在公共区块链网络中,L1 的原生Token是网络的货币。公共区块链网络内的产权和法律体系源自其共识机制、去中心化、安全性、社区性和价值。与国家类似,货币的强度与L1基础设施支持的经济/GDP以及访问网络内服务的Token需求相关。

根据从 Token Terminal 提取的数据,以太坊过去一年的“GDP”为 26 亿美元。我们按行业细分年收入如下:

以太坊目前在“GDP”和TVL(390 亿美元)方面领先其竞争对手。随着网络通过L2解决方案进行扩展,我们预计未来几年通过增强吞吐量和零知识隐私解决方案(“宽带”+“隐私”)带来的净新用例,经济机会(或 GDP)将呈指数级增长。

比较 ETH 需求与美元需求

为了扩展 ETH 作为货币的概念,我们分析了一种货币相对于其他货币的强度。美元因石油贸易需求与税收等结构性需求,在全球建立了强大地位,展现了货币的相对强度。美元本身没有任何效用,但我们需要他们来获得我们想要的东西。

我们在以太坊中看到了同样的模式。为了访问网络,必须用 ETH 支付计算资源费用。如果用户想要跨境发送稳定币,他们需要一些 ETH。要使用 DeFi 服务,需要使用 ETH 进行支付。要玩链上游戏,用户必须有一些 ETH。要铸造或购买 NFT,你最好有一些 ETH。此外,如果你想保护以太坊网络并获得收益,你需要持有一些 ETH。

我们甚至现在看到 ETH 用于通过 Eigen Layer 为技术堆栈的附加层提供经济安全——这是一种新兴的“重新抵押”解决方案,创造了对 ETH 的更多需求。

总而言之,我们看到 ETH 与美元等传统货币有相似之处。如果以太坊能够继续扩大其全球网络效应,考虑到访问网络内的服务的要求,我们认为用户和企业将会有强烈的持有该资产的需求。

下一个周期的到来

加密周期有三个主要驱动因素:

全球流动性/商业周期:利率和货币政策

创新周期:基础设施和应用程序的开发

比特币减半:比特币新发行量减半的日期(在这个周期中,我们从每天发行 900 个比特币减少到 450 个)

以比特币为基准,我们观察到过去三个周期在时间和价格走势方面具有显着的一致性:

每个周期峰值的回撤百分比:大约 80%

距周期底部的时间:距峰值 1 年

重新夺回历史新高的时间:2年

此外,每个周期都与 ISM 制造商 PMI 衡量的商业周期的周期性变化几乎完全一致,这也与全球流动性周期一致。

展望未来,我们相信,随着我们为 2024 年 4 月发生的下一次比特币减半做好准备,所有三个因素可能会再次一致。

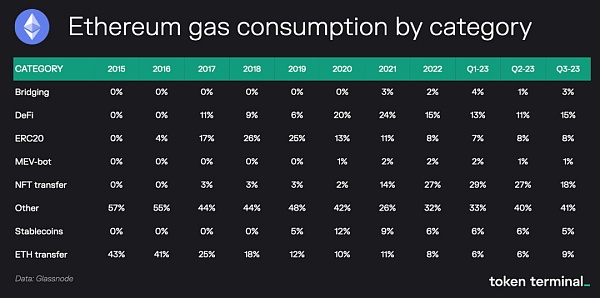

各年链上 Gas 消耗量

以上 Gas 消耗数据展示了以太坊作为计算基础设施的发展历程。值得注意的是,我们可以看到 2017 年引入了 DeFi,2019 年引入了稳定币作为支付和抵押品,2020 年引入了 NFT,2021 年引入了桥梁,这些都缓解了当时以太坊的拥堵。

未来,我们预计以太坊的大部分 Gas 消耗都来自L2决方案,随着成本的压缩,这将推动新用例的爆炸式增长。

模块化与集成化区块链的竞争

正如我们所知,以太坊作为一个“网络的网络”或“模块化”技术堆栈正在走向成熟和发展——其中结算(L1)和执行(L2)是分开的但又相互联系。

相比之下,Solana(排名第三)在整体或集成化架构中运行。在该架构中,结算和执行被放在一起。

我们认为以太坊和 Solana都有蓬勃发展的机会,有人将它们比作 Android 和 iOS。在这种情况下,以太坊更像是 Android,它重视模块化并运行在全球数百家制造商制造的许多不同设备上。Android 的灵活性和表现力使硬件开发人员能够制造从智能手机到电视的任何产品,而无需投资构建定制操作系统。

Solana 更像 iOS,因为它可以为用户和开发人员提供更加集成的体验,无缝连接不同的 L2 网络所需的复杂性。作为一个统一的网络,Solana 拥有比以太坊和 EVM 操作系统更低的交易成本和更高的吞吐量。这使得开发人员能够专注于交付有单一高性能平台的应用程序,而无需处理与不同网络之间的交易速度或互操作性相关的复杂性。它还可以消除桥接资产或处理不一致的钱包带来的麻烦,从而使用户的体验更加无缝。

但是,我们认为 Solana 等替代架构还有空间。我们认为,两者可以并存。

采用以太坊的催化剂和驱动因素

在短期内(2-3 年),我们看到可扩展性、隐私解决方案和监管清晰度将促进采用。从长远来看,以太坊在这十年有几个支持网络采用的有利因素:

1)开源技术:以太坊网络是web3运动的中心,作为开源技术的领导者,其创造了新的标准,通过可组合性和去中心化的特性推动着互联网下一代的迭代,并在创新和开发中受益于广泛的人才网络和快速迭代。

2)人口统计:目前,全球最大规模的人口统计变化正在塑造着美国和其他国家的未来,随着最后一批婴儿潮一代的逐步退休,年轻一代的观念和职业路径日益改变着整体格局。

3)钱包的全球分布:随着 web3 产品和服务的改进,我们认为由于该技术的开源性质以及任何拥有智能手机的人都可以参与这一事实,采用率可能会非线性扩展。据估计,如今全球 83% 的人口拥有智能手机(六年前这一比例为 49%)。

4)Token和价值的向外分配:加密网络如以太坊为新商业模式奠定基础,Token分配机制引导着价值分配,给予用户、创作者和供应方更多价值,实现更平等的所有权分配。

5)互联网文化:我们并没有忘记比特币没有首席执行官,没有董事会议室。没有销售或营销团队,并且没有“路线图”。然而,比特币估值达到 1 万亿美元的速度比历史上任何公司都要快。这也为像以太坊和其他 web3 网络带来了潜在的信念。

6)对机构缺乏信任:根据盖洛普民意调查,美国目前在有组织的宗教、最高法院、公立学校、报纸、国会、电视新闻、总统、警察、世界银行、国际货币基金组织、北约、欧盟、世界贸易组织等全球性机构都是在二战后建立的。历史显示着几十年的相对稳定后可能在短短十年内发生巨大改变。

7)宏观经济学:历史也表明长期债务周期的存在,当前处于末期,预示着可能出现地缘政治动荡,这种时期可能引发社会迅速变革,为 web3 和以太坊网络带来新的机遇。

8)L2扩展解决方案:以太坊的结算网络仍然缓慢昂贵,但L2扩展网络如Arbitrum、Optimism、Base和Polygon的增长,以及即将上线的EIP-4844,预示着交易吞吐量的大幅增长,促使以太坊迎来更广泛的应用和更优用户体验,可能在未来几年推动其用户量达到10亿。

9)金融创新:互联网颠覆了几乎所有可以想象的商业模式。但金融服务业商业模式相对不变。公共区块链被视为金融系统改革的推动力,特别是安永在以太坊上推出的名为 Nightfall 的基于隐私的 L2,有望成为机构迁移至公共区块链的催化剂。

10)新的互联网原生商业模式:正如我们在本文中所介绍的,以太坊通过引入用户控制的数据、智能合约、点对点交互和全球会计账本,实现了许多新的互联网原生商业模式。

结论

2021 年,加密货币总市值达到 3 万亿美元。尽管该领域存在波动,但我们认为加密货币正处于长期的、指数级的采用周期。因此,如果该行业遵循过去的增长模式,那么在下一个采用周期中,总市值可能会达到 10 万亿美元。根据简单的逻辑和历史数据,这个数字的 50% 以上可能会回归到比特币和以太坊(目前加密货币市场的 68.1%)。如果我们假设以太坊捕获 1-2.5 万亿美元,那么在下一个采用周期中,价格将在 8300 - 20800 美元的范围内。

毕竟以太坊展示了强大的网络效应、清晰的收入产生/价值的向外分配,以及“合并后”的高质量Token经济。核心团队已经展示了执行其路线图的能力,而以太坊生态系统/社区是我们在智能合约平台中见过的最强大的。

我们认为 ETH 代表了当今加密生态系统中最佳的风险调整回报潜力。投资者可以将 ETH 视为代表 web3 上看涨期权的指数基金。标准普尔 500 指数在新公司中轮换。以太坊轮换新的 L2、应用程序和协议。鉴于以太坊强大的网络效应,我们认为 ETH 的价值可能会随着 web3 的采用而增长,类似于谷歌、亚马逊和苹果随着互联网的采用而增长的方式。

Recently, the ecological rise of Bitcoin has been rapid, because some routes may overlap with the ecological growth of Ethereum, which has aroused the concern of some encryption communities. Will the ecological rise of Bitcoin really weaken Ethereum? In fact, it may not be true that Ethereum also has its own unique value. It is undeniable that the current development of the Internet has brought us endless richness, but it lacks two key elements: Internet users do not have digital property rights, and the Internet does not have a credible neutral, shared and secure global accounting system to record users without permission. And realize global trade on a shared account book, which are exactly the core values of blockchain. It advocates the revolution of the Internet on the way. The construction of Ethereum reflects the construction of the Internet. Bitcoin is the first public blockchain in the early days. If you want to use this new technological breakthrough to create a new application, you must start your own blockchain. For example, at first, the peer-to-peer naming system is a branch of Bitcoin network. This public blockchain era is similar to the Internet. In the early days, you had to host your own server to build a website. Ethereum was founded in 2006, and it was created as a geographical city with a public blockchain. Ethereum allows developers to use shared infrastructure to build applications based on blockchain, which is cheaper and more efficient. However, building applications for special use cases requires great flexibility. Entering and building specific application blockchains makes everyone start to build execution services on Ethereum, and Ethereum is the basic settlement infrastructure, so Ethereum is now. The network that becomes a network looks very similar to Taobao service just like the Internet. In addition, the enhanced scalability is being developed together with zero-knowledge proof, which brings privacy to the public blockchain, just like encryption to the Internet, thus realizing e-commerce. Investors in the business model of Ethereum should regard the Ethereum network as two different things to provide operating power for the network and transport it in a decentralized way. Line to create economic incentives for the native Ethereum computing network and accounting system as the basic layer for other enterprises to build applications, infrastructure data overview, the cumulative total of non-zero addresses has increased exponentially in the past years, and has increased by more than 100 million by the end of the year, which is higher than that of the previous quarter. In the third quarter, the average daily active address of Ethereum was about 10,000, which was similar to that of the previous quarter. However, with the market situation, a similar decline occurred in the cryptocurrency trough last year. In the third quarter, the average daily transaction volume of Ethereum increased slightly, and the network demand continued to exceed the supply. With the expansion of the network scale, the transaction volume of the network, such as and processing a larger proportion of transactions, increased more than in the past few years, highlighting the role of Moore's Law in Ethereum network. The average number of developers working in Ethereum stabilized in the third quarter. According to the developer report, the Ethereum ecosystem has more than. In the past two years, the number of active developers has increased by more than twice that of their nearest competitors. Please note that these figures may be underestimated because they do not reflect any contribution to the proprietary encryption business built on the Ethereum. As an indicator of the demand for block space on the Ethereum, the average daily usage is similar to the daily transaction volume. Recently, there has been a slight increase. Since the establishment of the network, the limit has doubled, and each increase is to meet the demand for block space. It is expected that this relationship will continue to develop further. Scheme expansion The average transaction cost of computing resources in Ethereum is USD in the third quarter, which shows that the shortage of block space leads to a sharp increase in the cost when the demand is high, while the transaction cost of the application programs expanded and utilized by the network through solutions and side chains, such as and, ranges from cents to cents. It is expected that the implementation will further reduce the cost in the fourth quarter, and the growth of pledge rate is very important for the healthy development of Ethereum network. This indicator tracks the pledge in the network. With the rapid increase of pledge participation, the holders have gradually shown a long-term prospect. At present, it is the only public blockchain network with positive real equity rate. The price encryption market is highly reflective. The price is closely related to the indicators on the chain, showing the sharp fluctuations every year since, such as the bottom price of $ in and the doubling growth peak in. The following article will provide a deeper valuation analysis. The daily trading volume continued to decline in the third quarter, compared with the same period last year, but it was not regulated. The certainty is related to the reduction of market-making business in the American market. At the same time, with the continuous cold winter of cryptocurrency, retail investors have lost interest in this field. In the application of Ethereum, it is $ billion, which is down from last quarter, but it is still twice as high as the nearest competitor. Another perspective is that the proportion of assets under management in smart contracts has reached a record high, showing the health status of managed assets, unit economic benefits, and the daily income of each active address increased in the second quarter compared with last quarter, but compared with the same period of last year. The decline shows that the daily cost growth of active users is consistent with the transaction cost growth, which shows that users are willing to pay higher fees when the network is congested because of the time value and sensitivity of online transactions. Through the solution, we can see that the user fees drop sharply. When this happens, the transaction volume is expected to increase exponentially. Although the economic and market structure of Ethereum is decentralized, its business model simply charges a small amount of calculation and settlement fees, and the network becomes more and more profitable with the expansion of applications. Next, This paper analyzes the financial situation of Ethereum in detail. The total revenue of Ethereum refers to the total cost paid by users on the network. It is expected that in the future, the application will pay the fees on behalf of users, covering peer-to-peer payment, loan trading platform, trading game experience, coinage, etc. Any application that uses the operation of Ethereum blockchain and uses the solution will eventually settle the data for the transaction of Ethereum's basic layer. Although the revenue in the third quarter is lower than that in the second quarter, the network still realizes the profit income cost. Table The amount paid to the supplier verifier, the verifier provides services for the network by approving the transaction and ensuring the network security, in which the user fee was burned in this quarter, and the remaining representative priority fee and cost incentive paid to the verifier on behalf of the network. After the merger in, the security fee of Ethereum was greatly reduced, which made the network profitable and provided compensation for the user fee for the verifier and passive holders. There are different views on the incentive. It is generally believed that it is a kind of fee paid to the verifier by the network, but its essence is different from that in the traditional sense, because the verifier does not directly pay the award. 比特币今日价格行情网_okx交易所app_永续合约_比特币怎么买卖交易_虚拟币交易所平台

注册有任何问题请添加 微信:MVIP619 拉你进入群

打开微信扫一扫

添加客服

进入交流群

1.本站遵循行业规范,任何转载的稿件都会明确标注作者和来源;2.本站的原创文章,请转载时务必注明文章作者和来源,不尊重原创的行为我们将追究责任;3.作者投稿可能会经我们编辑修改或补充。