Web3 银行协议 Fiat24 正在开启 DeFi 乐高游戏的无限遐想

Cointelegraph 近期报道了 Web3 银行协议 Fiat24 与 Safepal DApp 钱包的战略合作:Fiat24 为 Safepal DApp 钱包推出了 in-DApp 的 Web3 银行网关和虚拟加密支付 Visa 卡,以增强 DApp 钱包的易用性,进一步打通与现实世界的交互。

1. 将银行业务逻辑搬到链上之后,协议层能够与 DApp/DeFi 进行无缝衔接;

2. 为用户带来基于 U 本位的 Web3 链上银行服务;

3. 为 DApp/DeFi 带来法币业务的创新逻辑。

本文将先介绍 Fiat24 与 Safepal 的本次战略合作,再来进一步阐释 Web3 银行协议如何开启 DeFi 乐高游戏的无限遐想。

(Singaporean fintech launches USDC-powered Visa card with Swiss bank Fiat24)

一、无缝嫁接 Safepal DApp 钱包

3 月 8 日,由 Binance Labs 战略投资的 Safepal DApp 钱包已经接入 Fiat24 作为其默认的法币协议层,Safepal 钱包的用户可以通过 in-DApp 的 Web3 网银入口创建 Arbitrum 上的 Fiat24 链上银行账户,实现:

1. 基于 U 本位的链上银行服务,账户自托管,所有相关交易都安全、透明地记录在链上;

2. 钱包内加密资产 Crypto 与法币 Fiat 的出入金;

3. Fiat24 链上银行账户与实体银行账户的法币转账汇款,Euro/USD 的法币互换;

4. 接入虚拟加密支付 Visa 卡后,使用加密资产在现实世界中的无缝消费支付。

(https://www.safepal.com/en/bank)

Safepal 的创始人 & CEO Veronica Wong 表示:“在 SafePal 的钱包中创建 Fiat24 链上银行账户后,用户能够将钱包中的任何加密资产兑换成 USDC 存入 Fiat24 链上银行账户,虚拟加密支付 Visa 卡还能够与 Paypal、Google Pay、Apple Pay、Samsung Pay 等第三方支付进行链接,增强用户支付的便利性。”

二、Web3 银行协议 Fiat24

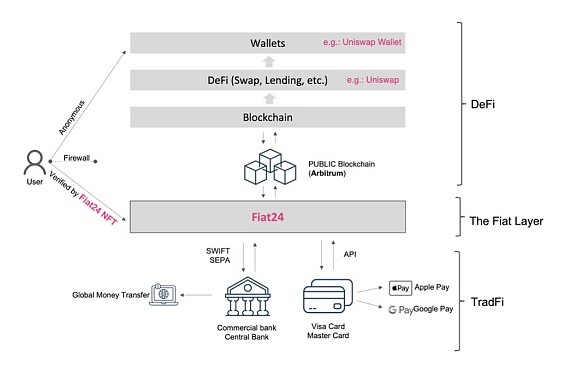

Fiat24 是一家获瑞士金融市场监管局(FINMA)发牌的金融科技公司,其推出了第一个将银行逻辑完全架构在公共区块链 (Arbitrum)上,完全由智能合约驱动的 Web3 银行协议,为用户创建一个链上银行账户,提供出入金、加密消费支付、储蓄、转账、换汇等一系列的 Web3 银行服务。

(Temperature Check - [Issue a Visa Card with Uniswap Logo ])

可以将Fiat24 想象成 DApp/DeFi 的法币协议层(Additional Fiat Layer for DApps)。在法币协议层,Fiat24 为通过 KYC 的用户创建链上银行账户(Cash Account),该账户一方面能够将 Web3 支付服务整合其中,例如用户通过链上银行账户直接实现出入金支付以及加密消费支付;另一方面,依托金融科技牌照,链上银行账户能与瑞士国家银行、欧洲中央银行和 VISA 支付网络直连,能够实现法币的储蓄、换汇、商家结算等传统银行服务。

Fiat24 将银行核心运营逻辑(Core Banking System)搬到链上,是 Fintech 在区块链创新的完美实践,最大程度地融合了区块链的去中心化账本技术,在增强便利性的同时也加强了安全性,避免了单点故障的风险。

更难能可贵的是,这种创新的做法获得了瑞士监管的认可,瑞士监管基于 Technology Neutral 的监管原则,保证 Fintech 公司在满足业务基础功能的前提下进行大胆科技创新。由此,Fiat24 一方面通过区块链实现了银行的账本记账,另外一方面通过 NFT 实现链上用户身份的 KYC,以满足反洗钱的要求。

Fiat24 的区块链银行架构将传统银行金融服务和 Web3 区块链创新无缝融合,获得了诸多顶级资本的青睐,同时也获得了 Qorus and Accenture 授予的 2022 最佳新兴银行(Neobanks & Specialized Players)的殊荣。

(Qorusand Accenture Announce Winners of 2022 Banking Innovation Awards)

三、为 DApp/DeFi 带来法币业务的创新逻辑

Fiat24 此前的创新在于将银行逻辑上链,并获得瑞士监管的认可。在这之后,Fiat24 的创新在于为 DApp/DeFi 开启新的法币业务逻辑。

由于 Fintech 牌照的限制,Fiat24 并不能够开展借贷业务,只能做吸储和支付业务。但是,这些限制反而为采用 Web3 银行架构的 Fiat24 带来巨大优势:

A. 基于 Debit Card 的全球发卡支付。Credit Card 本质上属于放贷,由于 Fiat24 牌照限制无法展业,并且违约催收压力巨大,一般局限于固定地域。而充值支付的 Debit Card 反倒能够实现全球网络的发卡支付,并且不存在违约问题。

对于那些希望将加密资产投入日常使用的用户来说,Fiat24 这种为 DApp/DeFi 提供出入金及加密支付解决方案的革命性能力是一种对传统支付体系的革新。

B. 无缝嫁接 DApp/DeFi。由于牌照限制无法开展借贷业务,但是并不妨碍 Fiat24 银行协议本身(Fiat Layer Protocol)能够直接自由嫁接在 DApp/DeFi 上,通过 DeFi 智能合约实现链上的借贷业务。

这里的重点在于:其作为协议能够为 DeFi 带来法币的业务逻辑。以最常见的金融活动为例:

1. 抵押借贷:Bob 提供加密资产 ETH 作为抵押品在 DeFi 平台上借稳定币,DeFi 协议可以直接调用 Fiat24 银行协议来做 USD 法币的出借;

2. 投资/质押生息:Alice 提供加密资产 ETH 去做质押生息,DeFi 协议可以直接调用 Fiat24 银行协议来做法币生息资产的发放,这真的能够躺赢?

3. 投资理财:Will 提供加密资产 ETH 直接投资 DeFi 协议的代币化证券 Coinbase,那么 DeFi 协议可以直接调用 Fiat24 银行协议,用法币去纳斯达克买股票。

(X@Fiat24)

将法币的逻辑加入 DeFi 的想象空间可以很大!同样,作为协议本身(Fiat Layer Protocol)能够直接自由嫁接在 DApp/DeFi 上的能力,亦能够帮助 Fiat24 丝滑接入 Blockchain Network,并带来巨大生态价值。

试想一下,中心化的 Metamask 钱包接入中心化的出入金 Moonpay,需要签订多少合同,需要经过多少部门讨论,需要多少领导签字?再试想一下,中心化的出入金 Moonpay 如何与去中心化的 DeFi 协议签订合同?DeFi 协议根本就没有法人主体,根本就没有公章。

而 Fiat24 银行协议与 DeFi Protocol 就不存在一点障碍,没有一点摩擦,just by one Click!

大家都没有法律上的强绑定,而是通过智能合约来一起做乐高游戏,这才是Web3的精髓。

四、写在最后

现在有两波人在做 Web3 Banking/Payment 的业务,一波是传统跨境支付的人,他们依然沿袭着传统跨境支付的思路,Crypto 只是多了一个币种,他们通过渠道手续费、会员费用订阅费赚钱,做的是现金流的生意;另外一波是 Web3 Native 的人,他们不太会去动现金流生意的脑筋,而是会直接用区块链去改造旧体制,释放新的活力,并且去拥抱社区生态,去做一些 Blockchain Network 的事,做的是生态的生意。

Recently, the strategic cooperation between banking protocol and wallet was reported. The bank gateway and virtual encrypted payment card were introduced for wallet to enhance the usability of wallet, and the interaction with the real world was further opened. After the banking business logic was moved to the chain, the protocol layer could be seamlessly connected to bring the standard-based online banking service to users and bring the innovative logic of legal tender business. This paper will first introduce this strategic cooperation with, and then further explain how the banking protocol can open the infinite reverie of Lego games. Sewing and grafting wallets: The wallet with strategic investment has been connected to the wallet with legal currency protocol layer as its default. Users can realize the self-hosting of online banking service accounts based on the online banking portal. All related transactions are recorded in the online wallet safely and transparently. The legal currency exchange of legal currency transfer and remittance between bank accounts and physical bank accounts on the gold chain uses encrypted assets in the real world after accessing the virtual encrypted payment card. The founder of seamless consumer payment said that after creating an online bank account in the wallet, users can convert any encrypted assets in the wallet into online bank accounts, and the virtual encrypted payment card can also be linked with third-party payment to enhance the convenience of user payment. The Second Banking Agreement is a financial technology company licensed by the Swiss Financial Market Supervision Bureau, and it has launched the first banking agreement that completely constructs the banking logic on the public blockchain and is driven by smart contracts for users. Building an online bank account provides a series of banking services, such as deposit and withdrawal, encryption, consumption, payment, savings transfer and exchange of foreign exchange. The imaginary legal tender agreement layer can be used to create online bank accounts for users who pass through the legal tender agreement layer. On the one hand, this account can integrate payment services, for example, users can directly realize deposit and withdrawal payment through online bank accounts and encrypt consumer payment. On the other hand, relying on financial technology licenses, online bank accounts can be directly connected with Swiss National Bank, European Central Bank and payment network. Even the traditional banking services, such as saving in legal tender and settlement of foreign exchange merchants, move the core operation logic of banks to the chain, which is the perfect practice of blockchain innovation. The decentralized accounting book technology of blockchain is integrated to the greatest extent, which not only enhances convenience, but also strengthens security and avoids the risk of single point of failure. What is more commendable is that this innovative approach has been recognized by Swiss supervision, which is based on the regulatory principles to ensure that companies can carry out bold projects on the premise of meeting the basic functions of business. On the one hand, technological innovation realizes the bookkeeping of banks through the blockchain; on the other hand, it seamlessly integrates traditional banking financial services with blockchain innovation through the blockchain banking architecture that meets the requirements of anti-money laundering, and has won the favor of many top capitals, and also won the honor of being awarded the best emerging bank. Third, it brings the innovative logic of legal tender business. The previous innovation was to link banks logically and gain the recognition of Swiss supervision. After that, the innovation lies in In order to open a new legal tender business logic, due to the license restrictions, it is impossible to carry out lending business, but these restrictions bring great advantages to the adoption of banking structure. The global card payment based on the license restrictions is essentially lending, and the pressure of default collection is generally limited to a fixed area, but it can realize the card payment of the global network and there is no default problem for those who want to put encrypted assets into daily use. For users, this revolutionary ability to provide deposit and withdrawal and encrypted payment solutions is an innovation to the traditional payment system. Due to the license restrictions, it is impossible to carry out lending business, but it does not prevent the bank agreement itself from being directly and freely grafted on the chain to realize lending business through smart contracts. The key point here is that as an agreement, it can provide encrypted assets as collateral for business logic that brings legal tender, taking the most common financial activities as an example. By using the stable currency agreement, you can directly call the bank agreement to lend money, invest and pledge interest, and provide encrypted assets to pledge interest-bearing agreements. You can directly call the bank agreement to issue money-bearing assets, which can really win the investment and wealth management, and provide tokenized securities for the encrypted assets direct investment agreement. Then the agreement can directly call the bank agreement, use French currency to buy stocks in Nasdaq, and the imagination of adding legal currency logic can be very large. Similarly, as the agreement itself, it can be directly grafted freely. The ability on the internet can also help smooth access and bring great ecological value. Imagine how many contracts need to be signed for centralized wallet access, how many departments need to discuss and how many leaders need to sign. Try again to think about how centralized deposit and withdrawal can sign contracts with decentralized agreements. There is no official seal at all, and there is no obstacle to bank agreements. Everyone has no strong legal binding, but through intelligent integration. Let's play Lego games together. This is the essence. At the end, there are two waves of people doing business. One wave is the traditional cross-border payment. They still follow the traditional idea of cross-border payment, but they make money through channel fees, membership fees and subscription fees. The other wave is the cash flow business. They are not very good at thinking about cash flow business, but will directly use blockchain to transform the old system, release new vitality and embrace the community ecology to do something ecological business. 比特币今日价格行情网_okx交易所app_永续合约_比特币怎么买卖交易_虚拟币交易所平台

注册有任何问题请添加 微信:MVIP619 拉你进入群

打开微信扫一扫

添加客服

进入交流群

1.本站遵循行业规范,任何转载的稿件都会明确标注作者和来源;2.本站的原创文章,请转载时务必注明文章作者和来源,不尊重原创的行为我们将追究责任;3.作者投稿可能会经我们编辑修改或补充。